permanent or whole life insurance

When it comes to financial planning, most Canadians think of RRSPs, TFSAs, or even real estate. But there’s one foundational tool that often flies under the radar – Permanent or Whole Life Insurance. For many Canadians, the term “life insurance” often brings to mind temporary coverage – a safety net for a specific period. But what if you’re seeking a more steadfast, lifelong financial solution? Enter permanent life insurance, a powerful and often misunderstood tool that offers more than just a payout. It’s not just about death benefits; it’s about building generational wealth, tax-free growth, and financial flexibility throughout your life.

Permanent Life Insurance provides coverage for the policyholder’s entire lifetime. The death benefit is guaranteed I.e. it provides guaranteed lifetime protection, as long as the premiums are paid. These policies usually have both a death benefit component and a cash value component (also known as cash surrender value). The cash value component grows over time and can be used as collateral for loans or withdrawn by the policyholder. Interest may accumulate in the savings component on a tax-deferred basis.

However, whole life insurance premiums are generally higher than term life insurance premiums.

What Is Permanent Life Insurance?

Permanent life insurance, also known as whole life insurance, is exactly what its name suggests—coverage that lasts your entire lifetime, provided you maintain premium payments. Permanent life insurance, which includes popular options like whole life and universal life insurance, provides coverage for your entire lifetime. Unlike term insurance, which expires after a set number of years, a permanent policy guarantees a tax-free death benefit to your beneficiaries, whether you pass away next year or on your 100th birthday.

But here’s where it gets interesting: it’s not just insurance, it’s a sophisticated financial instrument that combines death benefit protection with a powerful investment component. A portion of your premium payments contributes to a cash surrender value (CSV) that grows on a tax-deferred basis, offering benefits you can actually use while you’re alive.

The most compelling aspect? In Canada, the death benefit is delivered tax-free to your beneficiaries, making it one of the most efficient ways to transfer wealth to the next generation.

Types of permanent life insurance

1. Whole life:

- This is the most traditional type of permanent life insurance.

- The cash value can be borrowed against or used to pay premiums.

- Provides coverage for the entire lifetime of the life insured

- Premiums remain same throughout the payment period

- Has a set death benefit

- Builds up a cash surrender value (CSV) over time. When applicable, the policyholder may be entitled to receive payment of that CSV minus any surrender charges if the policyholder surrenders the policy prior to the death of the insured.

2. Term-100 (also called T-100 and Term-to-100):

- Provides coverage for the entire lifetime of the life insured for a set death benefit

- Has relatively lower premium than whole life

- Normally, these do not have a cash surrender value

- Policy matures at age 100 (i.e., premium payments stop at age 100 or upon death whichever is earlier, but life insurance coverage continues until the death of the policyholder)

3. Universal life :

- Universal life insurance is similar to whole life insurance, but it offers more flexibility such as:

- The policyholder can adjust the premiums and death benefit as needed.

- The policy also builds cash value, which can be used to pay premiums or withdrawn.

- Has a basic premium and an option to deposit more than the basic amount.

- Has a minimum death benefit with an option to increase the death benefit

- The policyholder decides how the savings component will be invested.

- Accumulated savings (and investments) are tax sheltered and form part of the death benefit (tax-deferred if funds are withdrawn prior to death).

- Universal life insurance tends to be less expensive than whole life insurance.

The choice between these options often comes down to your personal preferences regarding control, risk tolerance, and involvement in managing your policy. Traditional whole life appeals to those who prefer predictability, while universal life attracts Canadians who want more control over their investment outcomes.

6 Powerful Financial Benefits of Permanent Life Insurance

1. Tax-Advantaged Wealth Accumulation

One of permanent life insurance’s most attractive features for Canadian taxpayers is its unique tax treatment. By moving surplus, taxable funds into an exempt permanent life insurance policy, you could reduce the amount of taxes you have to pay during your lifetime.

The cash value within your policy grows tax-deferred. That means your money grows year after year without being taxed — similar to a TFSA, but without the contribution limits. This allows your money to compound more efficiently over time, potentially resulting in significantly higher long-term returns compared to taxable investment accounts.

🧠 Did You Know?

According to the Canadian Life and Health Insurance Association (CLHIA), over 22 million Canadians own some form of life insurance. Many are now adding Whole Life to create a living benefit.

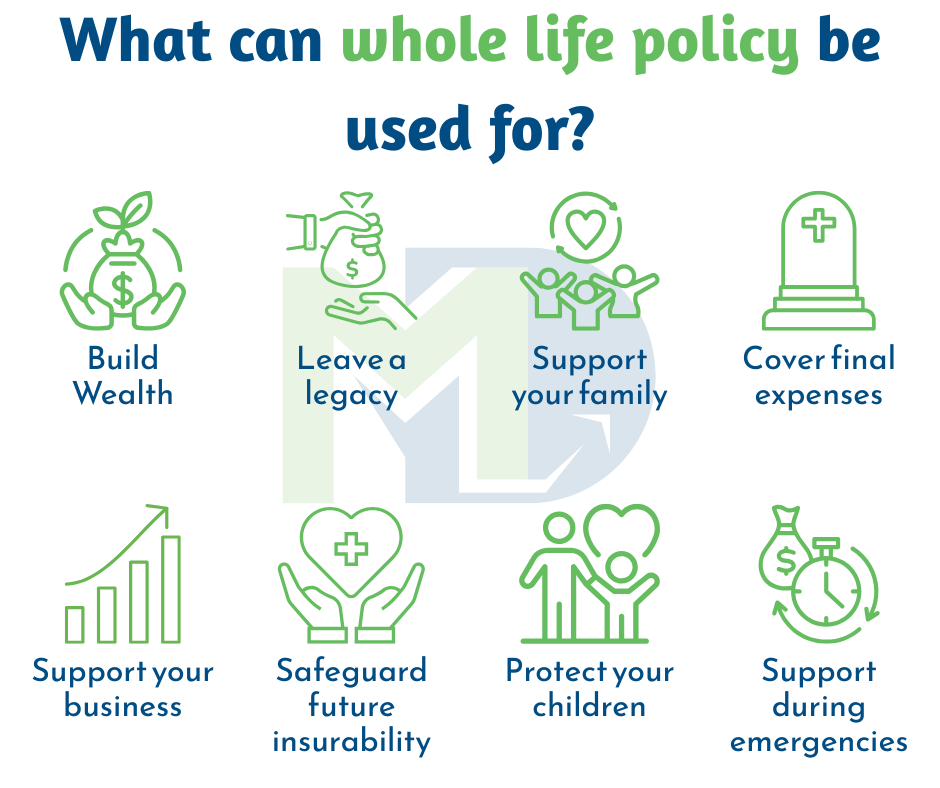

2. Living Benefits Through Cash Value Access

Perhaps the most misunderstood aspect of permanent life insurance is the ability to access your cash value while you’re alive. This isn’t just theoretical — it’s a practical financial tool that can provide liquidity for major life events, business opportunities, or financial emergencies.

You can typically access this cash value through policy loans or withdrawals, though it’s important to understand the implications. Withdrawals are generally taxable when the amount withdrawn exceeds the policy’s corresponding Adjusted Cost Basis (ACB).

When structured correctly, this cash value can be accessed smartly to fund:

- Retirement income

- Business opportunities

- Education for your kids

- Emergencies

This strategy is often called an “Insured Retirement Plan (IRP)” and is especially popular among high-income Canadians looking for a tax-efficient wealth solution.

3. Estate Planning Optimization

Whole Life Insurance allows you to pass on a tax-free death benefit to your heirs or beneficiaries. This makes it a powerful estate planning tool. Whether you want to help your children buy a home, leave a legacy, or fund a charitable cause, your policy ensures your vision lives on — without probate or capital gains tax.

👉 Tip: Pairing your Whole Life policy with a Joint-Last-to-Die option can further maximize your estate value, especially for couples.

This becomes particularly valuable for Canadians with substantial assets who want to ensure their loved ones receive the maximum benefit from their estate. The death benefit bypasses the probate process entirely when beneficiaries are named directly, providing immediate access to funds when they’re needed most.

4. Guaranteed Death Benefit Protection and fixed premiums

Unlike term insurance, which may become unaffordable or unavailable as you age, permanent life insurance guarantees that your beneficiaries will receive a death benefit regardless of when you pass away. With many whole life policies, your premium payments are fixed and will never increase. This certainty is invaluable for long-term financial planning, especially for families with dependents who will need ongoing financial support.

5. Hedge Against Future Insurability Issues

Life is unpredictable, and health issues can arise that make obtaining life insurance difficult or impossible. Permanent life insurance locks in your insurability, ensuring that you maintain coverage even if your health deteriorates. This benefit alone can be worth hundreds of thousands of dollars for individuals who develop serious health conditions later in life.

6. Potential for Dividends:

Participating whole life policies may earn dividends from the insurer’s profits. While not guaranteed, these are historically consistent and can be used to:

- Buy more insurance (paid-up additions)

- Reduce your premiums

- Take as cash

- Leave it to grow

Over time, this can significantly amplify your policy’s value.

Who Should Consider Permanent Life Insurance?

Permanent life insurance isn’t for everyone, but it’s particularly valuable for specific groups of Canadians:

- High-Income Earners who have maximized their RRSP and TFSA contributions often find permanent life insurance an attractive additional tax-shelter vehicle. The tax-deferred growth can complement their existing retirement planning strategies.

- Business Owners frequently use permanent life insurance for succession planning, key person coverage, and as a source of capital for business opportunities. The cash value can serve as collateral for business loans or provide funds for expansion.

- Parents with Dependent Children who need lifelong protection find permanent insurance provides peace of mind that term insurance cannot match. The guarantee that coverage will be in place regardless of future health changes is particularly valuable.

- Estate Planning Enthusiasts who want to maximize the wealth transferred to their heirs appreciate the tax-free nature of the death benefit and the ability to bypass probate.

Making the Decision: Key Factors to Consider

Choosing permanent life insurance requires careful consideration of several factors:

- Time Horizon – Permanent insurance becomes more valuable the longer you hold it. If you’re looking for coverage lasting longer than 20-30 years, permanent insurance often becomes cost-competitive with renewing term policies.

- Financial Capacity – You need sufficient income to comfortably afford the premiums without compromising other financial goals. Permanent insurance should complement, not replace, your retirement savings strategies.

- Risk Tolerance – If you’re uncomfortable with any investment risk, traditional whole life insurance might be preferable to universal life insurance with its investment options.

- Estate Planning Goals – The importance of leaving a legacy to your beneficiaries should factor into your decision. Permanent insurance excels at transferring wealth tax-efficiently.

When Permanent Life Insurance May Not Be Right for You

While permanent life insurance offers compelling benefits for many Canadians, it’s not suitable for everyone. Understanding the limitations and potential drawbacks is crucial for making an informed decision.

- Limited Financial Resources – If you’re struggling to maximize your TFSA and RRSP contributions, permanent life insurance premiums may not be your best financial priority. The higher cost compared to term insurance could prevent you from building your foundational retirement savings, which typically offer more flexibility and liquidity.

- Short-Term Insurance Needs – Canadians who only need coverage for 10-20 years (such as until a mortgage is paid off or children become independent) often find term insurance more cost-effective. The break-even point for permanent insurance typically occurs after 15-20 years, making it less attractive for shorter coverage periods.

- Preference for Investment Control – If you prefer direct control over your investments and want to choose specific stocks, ETFs, or mutual funds, the investment component of permanent insurance may feel restrictive. The returns, while tax-advantaged, may not match what you could achieve through direct market investing, especially in your younger years.

- Cash Flow Constraints – Permanent insurance requires consistent, long-term premium payments. If your income is variable or you anticipate financial challenges, the inflexibility of premium payments could create stress. Missing payments can result in policy lapse, potentially losing years of accumulated cash value.

- Immediate Liquidity Needs – Young professionals or those with high debt loads may find the cash value accumulation too slow to meet immediate financial needs. The early years of permanent policies typically show minimal cash value growth due to insurance costs and fees.

- Risk Tolerance Mismatch – Conservative investors who choose whole life insurance may find the guaranteed returns don’t keep pace with inflation over time. Conversely, aggressive investors might find universal life insurance investment options too limited compared to direct market investing.

- Complexity Concerns – Some Canadians prefer straightforward financial products. The multiple moving parts of permanent insurance—death benefits, cash values, tax implications, and various riders—can feel overwhelming for those who prefer simple, transparent financial tools.

Taking the Next Step

Permanent life insurance represents one of the most sophisticated financial tools available to Canadians, offering a unique combination of protection, tax advantages, and wealth-building potential. However, its complexity means that success depends largely on proper planning and implementation.

The key to unlocking permanent life insurance’s potential lies in understanding how it fits into your specific financial situation and long-term goals. This isn’t a decision to make quickly or without professional guidance.

The question isn’t whether permanent life insurance is right for everyone—it’s whether it’s right for you and your family’s unique circumstances.

Getting started with Whole Life Insurance isn’t as complex as it might seem—but it does require a thoughtful, tailored approach. Your policy should fit your financial goals, lifestyle, and future plans, not the other way around.

Here’s how the process typically works when you work with an experienced, licensed advisor in Canada:

🔍 Step 1: Needs-Based Analysis

We begin with a comprehensive review of your financial situation. This includes:

- Your current income and expenses

- Family or dependents you want to protect

- Debt obligations (mortgage, lines of credit, etc.)

- Retirement and estate goals

- Business ownership or succession needs

Using tools like the Expert Financial Advice (EFA) Platform, we calculate the right coverage amount and help you see how insurance integrates with your overall wealth plan.

📊 Step 2: Custom Policy Design

Based on your profile, we design a Whole Life Insurance plan that considers:

- How long you want to pay premiums (e.g., 10-pay, 20-pay, or for life)

- How much guaranteed cash value you want to build

- Whether you qualify for participating dividends

- Riders or add-ons like critical illness or disability waivers

You’ll see visual projections of cash value growth, death benefit increases, and how much you can access over time.

✅ Step 3: Underwriting and Approval

Once you’re ready, we guide you through the application and underwriting process (including medical review, if needed). The good news is that some companies now offer simplified or non-medical underwriting for smaller policies or younger applicants.

🛠️ Step 4: Ongoing Review and Adjustments

Your life changes—and your policy can adapt with it. We’ll review your plan regularly to make sure it continues to support:

- Growing your estate

- Funding business or family needs

- Maximizing your retirement cash flow

- Taking advantage of tax law changes

📞 Ready to Take the First Step?

🔒 Book your free 1-on-1 consultation today and get your customized Whole Life Insurance blueprint—based on your unique needs, goals, and future dreams.

👉 Fill out the form to get started. Your future self will thank you.