Life Insurance

Life is unpredictable, and while we hope for the best, planning for the unexpected is essential. Life insurance is a vital financial tool that provides security for you and your family. Though often overlooked, it’s a small investment that brings lasting peace of mind and helps you truly “own your future.”

What Is Life Insurance?

Life insurance is a contract between you and an insurance company that provides financial protection for your beneficiaries in the event of your death. In exchange for regular premium payments, the insurance company guarantees a tax-free death benefit to your designated beneficiaries. This financial safety net can help cover funeral expenses, pay off debts, replace lost income, and secure your family’s future.

Why life insurance matters?

The statistics are sobering: nearly 40% of American families would face financial hardship within six months if the primary breadwinner passed away. Life insurance bridges this gap, providing peace of mind and financial security during an already difficult time.

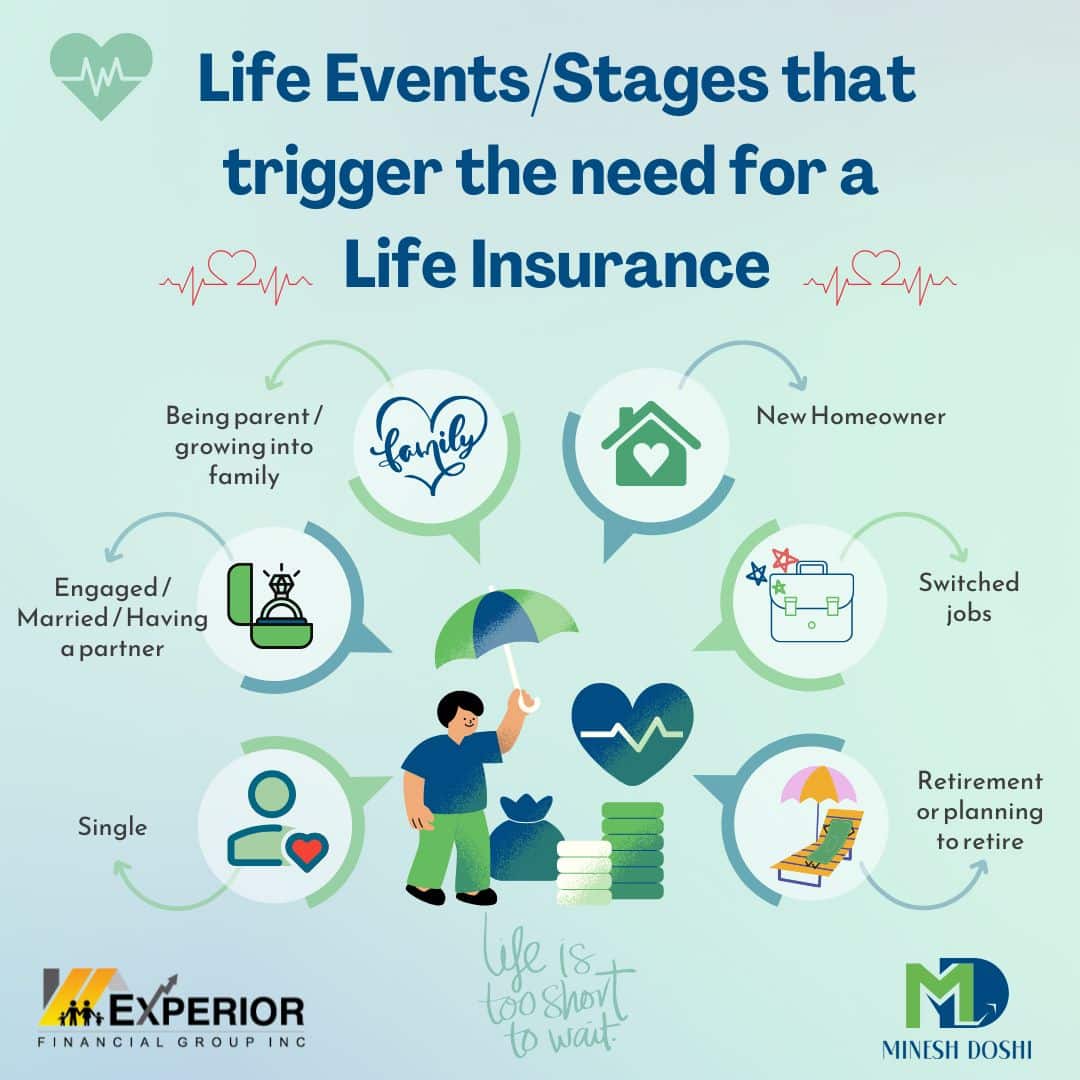

Consider life insurance if you have:

- A spouse or partner who depends on your income

- Children or dependents who rely on your financial support

- Outstanding debts like a mortgage, car loans, or credit cards

- Business obligations or partnerships

- Charitable giving goals

- Estate planning needs

Features of Life Insurance

- Death Benefit Payout: All policies provide a death benefit payout to the policyholder’s beneficiaries in case of the policyholder’s death. The amount of the death benefit payout depends on the policyholder’s chosen coverage amount and the type of policy.

- Premiums: Premiums are the amount paid by the policyholder to the insurance company for the policy coverage. The premiums vary depending on the policy type, coverage amount, policyholder’s age, and health status.

- Cash Value Component: Permanent life insurance policies have a cash value component that grows over time based on the policyholder’s premium payments and the investment performance of the underlying investments. The policyholder can use the cash value component as collateral for loans or withdraw it.

- Flexibility: Universal life insurance policies provide policyholders with the flexibility to adjust premiums, death benefit, and cash value component over time. This flexibility allows policyholders to adjust their policies to meet their changing financial needs.

Key Benefits of Life Insurance

- Financial Security for Loved Ones: Replaces your income, ensuring your family can maintain their standard of living and meet ongoing expenses without financial strain.

- Debt Protection: Help pay off outstanding debts like mortgages, credit cards, and other loans, preventing your family from inheriting financial burdens.

- Tax-Free Death Benefits: Life insurance proceeds are generally received tax-free by beneficiaries, providing the full benefit amount when it’s needed most.

- Estate Planning Tool: Can help equalize inheritances among beneficiaries, pay estate taxes, and ensure your legacy is preserved according to your wishes.

- Business Continuity: For business owners, life insurance can fund buy-sell agreements, cover key person losses, and ensure business operations continue smoothly.

- Flexible Coverage Options: Modern life insurance policies offer flexibility to adjust coverage amounts, payment schedules, and even access cash value during your lifetime.

Types of Life Insurance

Term Insurance

Term life insurance is the most basic type of life insurance policy. It provides coverage for a specified period, usually ranging from 5 to 30 years. In case of the policyholder’s death within the policy term, the beneficiaries receive a death benefit payout. The premiums for term life insurance are relatively low compared to other types of life insurance policies. However, the policy does not have any cash value or investment component.

Permanent or Whole Life Insurance

Permanent Life Insurance provides coverage for the policyholder’s entire lifetime. The death benefit is guaranteed I.e. it provides guaranteed lifetime protection, as long as the premiums are paid. These policies usually have both a death benefit component and a cash value component (also known as cash surrender value). The cash value component grows over time and can be used as collateral for loans or withdrawn by the policyholder. Interest may accumulate in the savings component on a tax-deferred basis.

Universal Life Insurance

Universal life (UL) insurance is a type of permanent life insurance that, like other permanent insurance, has a cash value element and offers lifetime coverage as long as you pay your premiums. Unlike whole life insurance, universal life allows you to raise or lower your premiums within certain limits, and it can be cheaper than whole life coverage.

How Much Life Insurance Do You Need?

Determining the right amount of coverage depends on your unique situation. Consider these factors:

- Income Replacement: A common rule of thumb is 10-12 times your annual income or until your dependents become adults, but this varies based on your family’s needs and other financial resources.

- Debt Coverage: Add up all outstanding debts including mortgages, car loans, credit cards, and student loans that would need to be paid off.

- Future Expenses: Consider future costs like children’s education, spouse’s retirement needs, and final expenses.

- Existing Coverage: Subtract any existing life insurance through employers or other policies to avoid over-insuring.

- Available Assets: Factor in savings, investments, and other assets that could provide financial support.

Factors Affecting Life Insurance Costs

Age

Younger individuals pay lower premiums.

Health

Healthier individuals pay lower premiums. Medical exams and health questionnaires help determine rates.

Coverage Amount

Higher death benefits result in higher premiums, but the cost per dollar of coverage often decreases with larger policies.

Policy Type

Term insurance is initially less expensive than permanent insurance, but costs vary significantly between policy types.

Gender

Women typically pay slightly lower rates due to longer life expectancy.

Lifestyle

Smoking, dangerous hobbies, and risky occupations can increase premiums or require specialized coverage.

Common Life Insurance Myths

Actually, youth is an advantage in life insurance. You’re likely healthier and will lock in lower rates for life with permanent coverage.

Term life insurance is surprisingly affordable. A healthy 30-year-old can often get $500,000 of coverage for less than $30 per month.

Employer coverage is often limited and not portable if you change jobs. Personal coverage ensures continuous protection.

Even single individuals may have debts, aging parents, or charitable intentions that life insurance can address.

Many health conditions don’t prevent you from getting coverage. Simplified issue and guaranteed acceptance policies are available for those with serious health concerns.

Why chose Minesh as your Independent Broker?

Unbiased Advice

I represent multiple insurance companies and can objectively compare options to find the best fit for your needs and budget.

Service philosophy

My service philosophy is built on transparency, accessibility, and genuine client advocacy. I provide free, no-obligation consultations coupled with pressure-free, honest guidance that prioritizes your interests over sales quotas. You’ll never experience pushy sales tactics or feel pressured to make immediate decisions.

No Additional Cost

Insurance companies pay broker commissions, so working with me doesn’t cost you anything extra.

Access to Multiple Carriers

Different companies excel in different areas. I can access specialized products and competitive rates across the market.

Personalized Service

You’ll work directly with me throughout the process, ensuring personalized attention and ongoing support. Every plan I develop is personalized to suit your individual needs, budget considerations, risk tolerance, and long-term financial goals.

Advocacy

If issues arise with your policy, I advocate on your behalf with the insurance company.

Getting Started

Protecting your family’s financial future doesn’t have to be complicated. The first step is understanding your needs and exploring your options. Every day you wait, you’re potentially exposing your family to financial risk.

I’m here to guide you through the process, answer your questions, and help you make an informed decision that provides peace of mind for you and security for your loved ones.

Don’t wait until it’s too late. Your family’s financial security is too important to leave to chance. Let’s work together to find the right life insurance solution for your unique situation.

Ready to get started? Fill out this short form or Contact me today for a free, no-obligation consultation. Together, we’ll create a life insurance strategy that protects what matters most to you.